| ||||||||||||||||||||||||||||||

Showing posts with label inflation. Show all posts

Showing posts with label inflation. Show all posts

Friday, September 9, 2011

Marc Faber: Gold is Dirt cheap.

Thursday, June 2, 2011

More on inflation

This is a continuation of the last post. After looking at it, it seemed to me that the interpretation of the chart was a little oversimplified, and that was because the numbers had changed so much over the 18 years of the study that log scale would be more enlightening. No easier said than done (OK, a little easier said). Here is the same graph in log scale:

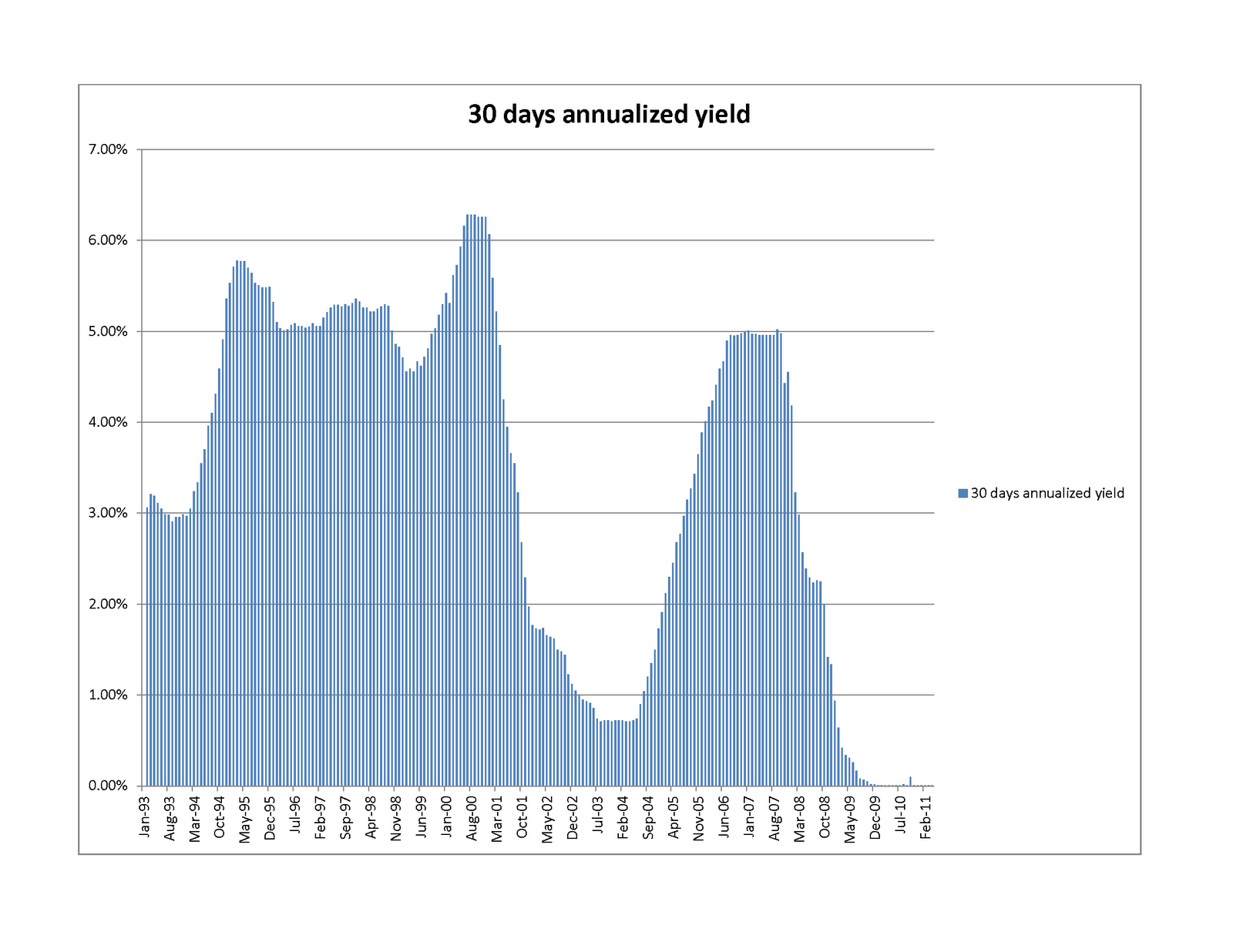

In this form, it seems clear that (other than some cyclical behavior) there was essentially no commodity price inflation from the beginning of the study (January 1993) until the end of 2001 -- beginning of 2002 (also known as the Dot Com crash). In those nine years, a conservative saver seems to have actually increased the purchasing power of his bank account quite considerably (by around 50%, in real terms). During that golden age (which we can call the Age of Clinton), there was a combination of the peace dividend, considerable technological innovation, a gridlocked government which actually managed to run a surplus, and fairly conservative fiscal policy. The chart below shows prevailing money market rates, which are closely tied to Fed Funds:

In this form, it seems clear that (other than some cyclical behavior) there was essentially no commodity price inflation from the beginning of the study (January 1993) until the end of 2001 -- beginning of 2002 (also known as the Dot Com crash). In those nine years, a conservative saver seems to have actually increased the purchasing power of his bank account quite considerably (by around 50%, in real terms). During that golden age (which we can call the Age of Clinton), there was a combination of the peace dividend, considerable technological innovation, a gridlocked government which actually managed to run a surplus, and fairly conservative fiscal policy. The chart below shows prevailing money market rates, which are closely tied to Fed Funds:

You will note that the "Greenspan put" coincides almost exactly with the end of the golden age (marked somewhat more memorably by the terrorist attacks of 9/11/2001). The massive money printing, did not wait to make itself be felt: tgold prices rise at a 1.5% a month clip -- the log scale graphs are amazingly linear (the F statistic, which shows the strength of the trend, is around 5000), commodity basket prices rise somewhat slower (1.1% a month clip), with more variability. During this period (the last ten years, approximately), our hapless saver's money market account gains around 20% in nominal dollars, but loses around 70% of its commodities purchasing power. Being no fool, our saver decided to invest her hard-earned dollars in real estate, but imagine her dismay when that investment did about as well (or poorly) as her neighbor's money market account (the graph below shows the change in the Case-Shiller index versus the Money Market account. You will see that nominally, Case-Shiller outperformed the money market account by around 15%, but all of that and more was eaten up by transaction costs, property taxes, and so on. I am only viewing housing as an investment, so am not counting the savings of rent or the mortgage tax deduction.

You will note that the "Greenspan put" coincides almost exactly with the end of the golden age (marked somewhat more memorably by the terrorist attacks of 9/11/2001). The massive money printing, did not wait to make itself be felt: tgold prices rise at a 1.5% a month clip -- the log scale graphs are amazingly linear (the F statistic, which shows the strength of the trend, is around 5000), commodity basket prices rise somewhat slower (1.1% a month clip), with more variability. During this period (the last ten years, approximately), our hapless saver's money market account gains around 20% in nominal dollars, but loses around 70% of its commodities purchasing power. Being no fool, our saver decided to invest her hard-earned dollars in real estate, but imagine her dismay when that investment did about as well (or poorly) as her neighbor's money market account (the graph below shows the change in the Case-Shiller index versus the Money Market account. You will see that nominally, Case-Shiller outperformed the money market account by around 15%, but all of that and more was eaten up by transaction costs, property taxes, and so on. I am only viewing housing as an investment, so am not counting the savings of rent or the mortgage tax deduction.

Since the move into housing was borne of desperation with the performance of the simpler ways of saving, it is not at all surprising that the returns are similar, though as we all know, the disruption caused by the fact that real estate investment is very far from risk free (as everyone now knows) has been rather considerable.

It is always harder to determine causality than correlation, so the graphs by no means prove that that monetary policy caused the end of the Golden Age of Clinton and the implosion of our savings, but they do provide some food for thought, I hope.

Since the move into housing was borne of desperation with the performance of the simpler ways of saving, it is not at all surprising that the returns are similar, though as we all know, the disruption caused by the fact that real estate investment is very far from risk free (as everyone now knows) has been rather considerable.

It is always harder to determine causality than correlation, so the graphs by no means prove that that monetary policy caused the end of the Golden Age of Clinton and the implosion of our savings, but they do provide some food for thought, I hope.

Wednesday, June 1, 2011

What is inflation really, or what's the use of gold?

Those who have read this previous post probably (and understandably) wonder how reasonable the Alternative CPI measure is. After all, it seems to indicate that our cost of living has increased almost four-fold since 1993, which seems rather steep (mostly since for only very few of us has our income increased four-fold in the same period). There is no question that the official numbers are seriously gamed (see this note, or this), but that, in and of itself mean that the alternative numbers are right. My personal view is that the Alternative CPI measure is more a measure of inflation (that is, the debasement of the dollar) than the actual CPI growth -- the latter tends to be smaller than the former, since the money-printing is offset by technological progress, which causes computers to drop from $6000 in 1981 to $150 at Walmart in 2011 (the latter computer also being several orders more powerful), and your car's fuel consumption to go from 8mpg in the 1960s to 40mpg today.

A good proxy for inflation is, however, provided by prices of commodities (still not perfect, since exploration and mining also have made considerable strides), and since a representative basket of commodities is rather cumbersome to hold, a good proxy for one is gold -- indeed, gold is almost miraculously convenient -- it is compact, it does not degrade, and it saves you from buying shares of oil tankers parked off Singapore.

The above seems counterintuitive (after all, we have all heard of the gold bubble, but [relatively] few of us have heard of the the wool, rice, natural gas, or any one of the many other possible commodities bubbles. Well, luckily for us, the IMF maintains a commodities price index, so we can compare and contrast. Here is the requisite chart:

A good proxy for inflation is, however, provided by prices of commodities (still not perfect, since exploration and mining also have made considerable strides), and since a representative basket of commodities is rather cumbersome to hold, a good proxy for one is gold -- indeed, gold is almost miraculously convenient -- it is compact, it does not degrade, and it saves you from buying shares of oil tankers parked off Singapore.

The above seems counterintuitive (after all, we have all heard of the gold bubble, but [relatively] few of us have heard of the the wool, rice, natural gas, or any one of the many other possible commodities bubbles. Well, luckily for us, the IMF maintains a commodities price index, so we can compare and contrast. Here is the requisite chart:

Some explanation might be in orer: The very smooth red line shows how many dollars you would have were you to invest $1 in a money market account in January of 1993. The almost-as-smooth green line shows how many of those dollars you would need according to the Alternative CPI computation to purchase a basket of goods worth $1 in Jan 1993. The jagged purple line shows how many of those dollars you would need to purchase however much gold you could buy for a dollar in January of 1993, while the really jagged light blue line shows the same for a dollars worth of a commodity basket. The conclusions, at least to me, are:

- The Alternative CPI seems, as advertised, to be a good measure of inflation (and is, therefore, a bit of an overestimate of the actual price inflation).

- There is no gold bubble (a conclusion also drawn in a previous post from other data).

- Gold (in addition to its compactness) is a better gauge of monetary inflation than the commodities basket (witness the huge volatility in the latter starting in late 2007 or, for that matter, just in this May.

- The red line (your risk free return) was added just to make the chart more depressing. Unfortunately, it has achieved its goal brilliantly.

Subscribe to:

Posts (Atom)